QAU Alert 2015-01: ASEAN Mutual Recognition Arrangement on Accountancy Services Impact on the Philippine Accounting Profession

INTRODUCTION

The Association of Southeast Asian Nations (ASEAN) was formed by Indonesia, Philippines, Singapore and Thailand in 1967. From 1984 to 1999, Brunei Darussalam, Cambodia, Lao People’s Democratic Republic, Myanmar, and Viet Nam joined the Association. The main objective of the ASEAN was to foster regional peace and security. As time progressed, it was made to facilitate also economic integration and cooperation. This led to the 1992 Free Trade Area (AFTA).

While the change in the country’s economic policies, such as tariffs and other taxes paved way for the manufacturing and trading industries, the ASEAN pioneered most of the MRAs on professionals, including Accountancy. Other MRAs include Engineering Services, Nursing Services, Surveying Qualifications, Architectural Services, and others.

SIGNIFICANT PROVISIONS

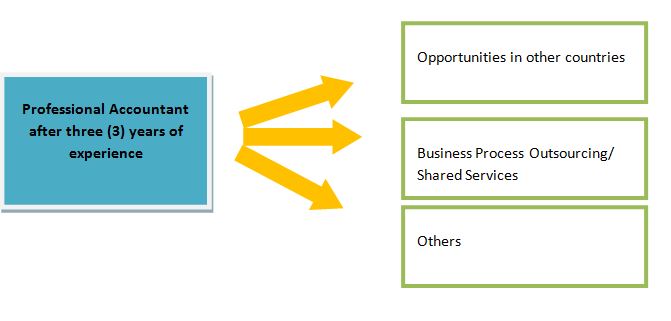

Under Article 4 Recognition, Qualifications, and Eligibility, a Professional Accountant is eligible to apply through the Monitoring Committee of his or her Country of Origin, to be registered as an ASEAN Chartered Professional Accountant (ACPA) on the ASEAN Chartered Professional Accountant Register (ACPAR).

The process is shown below:

Under Appendix II ASEAN Chartered Professional Accountants Guidelines on Criteria and Procedures the eligibility of a Professional Accountant for designation as an ASEAN Chartered Professional Accountant are determined to be the following:

- Completed an accredited or recognized accountancy degree or program, or assessed and recognized as possessing the equivalent

- Been assessed with their own jurisdiction as eligible for professional accountancy practice

- Gained a minimum of three years post qualifying practical experience

- Complied with the Continuing Professional Development (CPD) policy at a satisfactory level

- Registered ASEAN Chartered Professional Accountants (ACPA) must agree to the Codes of professional conduct and Accountability.

The ASEAN Chartered Professional Accountant can then apply as a Registered Foreign Professional Accountant (RFPA) shall be permitted to work in the Host Country, not as an independent practice, but in collaboration with designated Professional Accountants in the Host Country within such area of his own competency as may be approved by the Host Country’s National Accountancy Body (NAB) and/or Professional Regulatory Authority (PRA) of the Host Country.

IMPACT ON THE PHILIPPINE ACCOUNTING PROFESSION

In the Philippines, the Professional Regulatory Authority (PRA) and the National Accountancy Body (NAB) are the Professional Regulation Commission (PRC) and the Board of Accountancy (BOA), and the Philippine Institute of Certified Public Accountants (PICPA), respectively. These local bodies regulate the Accounting Profession.

The start of one’s accounting profession is upon graduation from the Bachelor of Science in Accountancy. However, in order to be qualified as an ACPA, one has to be a Certified Public Accountant.

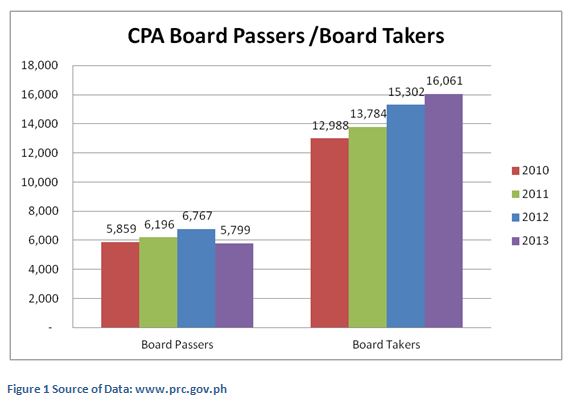

The statistics of the Board takers and the Board passers are shown in the diagram below:

The average passing rate of accounting graduates in the CPA Board is 43%. Board passers generally take the route of applying in auditing firms. Auditing firms serve as training ground to provide the Professional Accountant adequate experience in accounting and other related services.

According to the Securities and Exchange Commission (SEC) SRC Rule 68.1, corporations that meet the criteria stated therein are required to submit audited financial statements. The total accredited auditing firms as of August 31, 2014 is 109, only 25 are accredited as Group A. This provides limited supply on an increasing demand to cater t SEC registered corporations.

Out of the CPA Board passers, a substantial percentage goes to private industry, education and government, instead of auditing firms.

IMPACT OF MRA TO THE PUBLIC PRACTICE

Based on Figure 1, from the year 2010 to 2013, the Philippines produced a total of 24,621 Certified Public Accountants. The average turnover of an employee in public practice is three years. Hence out of those 24,621, only a small percentage will be remaining as senior auditors in the 109 auditing firms.

Below are the several threats to the supply for public practice:

In the year 2010 alone [no other available data from www.poea.gov.ph], 725 accountants were deployed in several countries. Out of the 725 accountants only 14 were deployed to ASEAN Member States. Perhaps, the MRA will open more opportunities for the Philippine Professional Accountant. However, this may also impact the supply of external auditors in the country.

Counter-measures can be placed in order to decrease the risk. One suggestion in mind is to increase the pay grade scale of an external auditor. However, given the economies of scale, this is less likely to take place as it means a substantial increase in the professional fees charged to the SEC registered corporations.

The other suggestion is to take advantage of the opportunity. ASEAN Professional Accountants can practice in different member states in collaboration with the Professional Accountants in the Host Country. The Philippine auditing firms can outsource its Professional Accountants to other auditing firms in the Member States at a lower cost.

In addition, the Philippine Auditing firms, in collaboration with the Host Country’s auditing firms, can offer its services and expertise, such as but not limited to transition to the International Financial Reporting Standards, Internal Auditing, and Group consolidation (if the Parent or branch is in the Philippines).

One thing is for sure, the MRA’s impact on the Philippine accounting profession and public practice depends on how we plan and react to the integration of ASEAN member states.